How to Get a Personal Loan & What to Consider

All over the world, personal loans are hugely popular. They can be obtained from any bank, credit union, or online lender and used for any legitimate private purpose – from buying a car to paying for a wedding trip.

However, taking a loan from the first lender you meet without knowing the specifics of this type of borrowing is a wrong decision, as you might choose an offer with a high APR or additional fees. In this article, let’s understand all the features of personal loans and discuss how to get them quickly and on favorable terms.

What Personal Loans Are?

A personal loan can be any installment loan you get for personal purposes and repay in fixed payments over one or more years. Most of these loans are unsecured, which means that they do not require any collateral.

However, users with low FICO scores can also choose secured personal loans to get a larger amount at a lower interest rate. Typically, you can borrow between $1,000 and $100,000 for two to 10 years under these offers.

Typical interest rates from online lenders can be as high as 36%, while banks and credit unions have 25%. Obtaining a personal loan is relatively easy and quick, so many lenders promise to transfer funds to your account in as little as 1-3 days.

However, sometimes the process takes up to 30 days, especially if you choose secured personal loans (because of the appraisal stage of the property provided as collateral).

Types of Personal Loans

Since personal loans can be used for any legitimate purpose, they are rarely separated by this factor. Instead, there are two types of these loans: secured and unsecured, depending on whether you need to provide collateral to obtain the funds.

Secured Personal Loans

All lenders want their borrowers to repay, so they try to check how reliable and creditworthy their new clients are. To provide loans quickly, they don’t contain much information about borrowers but often look at just a few indicators, a key one being a FICO score.

If your credit rating is low, you have insufficient income, or you already have a high debt-to-income ratio, it will be challenging to get a loan as the lender may assess you as a risky borrower.

In such a situation, you can apply for a secured loan and provide collateral (car, house, investment account, etc.) to guarantee that you will repay the borrowed funds on time. Of course, taking out such loans is very risky.

Therefore, it is worth doing so only when you are sure that you will be able to cope with the monthly payments and comply with the terms of the agreement.

If suddenly you cannot pay back the loan within the specified period, you will have to hand over the property presented as collateral to the lender so that he can sell it and recoup the loss.

Secured loans have many advantages. With them, you can get more money for a longer term and a lower interest rate, regardless of your FICO score.

However, their main disadvantage, the risk of losing your collateral, cannot be ignored. Consider whether you have other options that won’t be much more expensive but will allow you to have less risk, such as unsecured personal loans.

Unsecured Personal Loans

Unsecured loans differ from the last option because they do not require collateral, which is their main advantage. However, because lenders have no guarantee that you will pay back all the funds on time, they set higher interest rates and allow you to borrow a smaller amount of money.

Of the other pluses of this option, it is essential to note the speed of getting funds into your account; it can be up to one business day. However, it is also worth remembering that such loans are more challenging to obtain because of the higher requirements of lenders.

To have a better chance of getting your application approved, you need to have good credit, official employment, and regular income. If you fail to repay such a loan, you won’t risk the collateral, but your credit history will be ruined.

In addition, creditors can turn it over to debt collectors, which will also appear on your credit report. As with secured personal loans, you should only choose this option if you are confident that you can repay all of your borrowed funds on time.

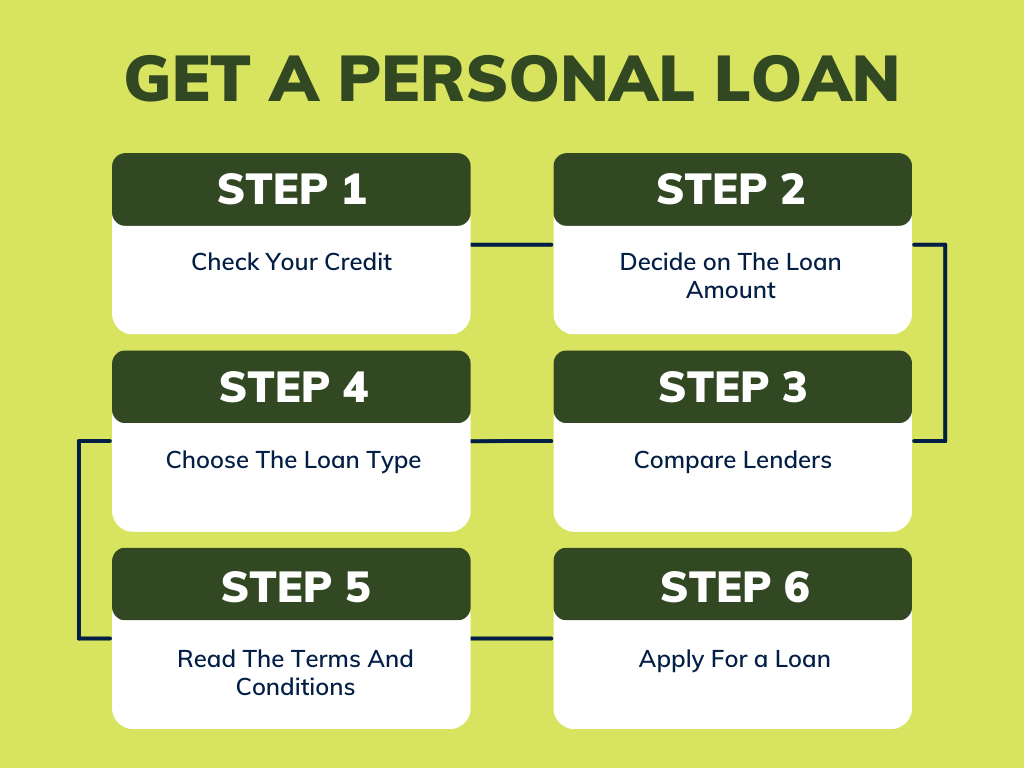

How to Get a Personal Loan: Step-by-Step Guide

Getting a personal loan is a simple process if you prepare for it and know which steps you must go through. We have explained each step in more detail below.

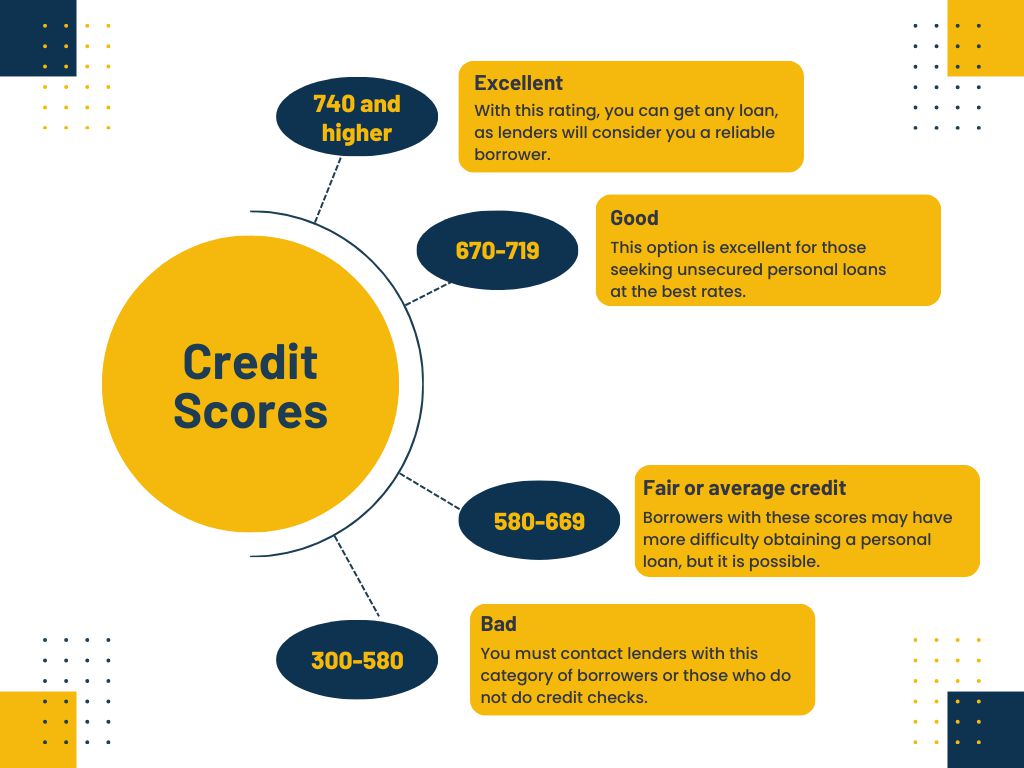

Check Your Credit

At least once a year, you should request a free copy of your credit report from the credit bureau to know your score precisely. You should also do this before you take out a loan so that you only go to lenders who specialize in working with the kind of borrower you are. Lenders generally divide the FICO score into the following categories:

- 740 and higher: Excellent. With this rating, you can get any loan, as lenders will consider you a reliable borrower.

- 670-719: Good. This option is excellent for those seeking unsecured personal loans at the best rates.

- 580-669: Fair or average credit. Borrowers with these scores may have more difficulty obtaining a personal loan, but it is possible.

- 300-580: Bad. You must contact lenders with this category of borrowers or those who do not do credit checks.

The lower your score, the less favorable your loan terms will be. So if you can get a loan in 6-12 months rather than now, you’re better off devoting that time to improving your credit history and score to save thousands of dollars in lower interest rates later.

Decide on The Loan Amount

Every financial institution’s first question is how much you want to borrow. The loan amount affects not only your monthly payments but also the interest rate and repayment period, which is why it is so important to get it right. Borrowers usually make one of two mistakes:

- They do not calculate how much they need to borrow and try to get the biggest loan possible, which makes them unable to cope with the monthly payments.

- Ask the financial institution precisely what they need to cover expenses, leaving no reserve for unforeseen factors.

The safest way to calculate that you should use is to add a 15% contingency fee to the amount you need. Also, remember that many personal loan lenders charge an origination fee of up to 10%, which you should also consider when calculating the amount.

In total, if you want to borrow $5,000 to buy home electrical appliances, you need to add 15% (for insurance, additional accessories, and shipping) and up to 10% more (origination fee). So, in total, you need to ask for $6250.

Choose The Loan Type

As we clarified above, two main types of personal loans are secured and unsecured. Therefore, we recommend you approach lenders willing to lend you money without providing collateral so you do not risk your property.

In this situation, you must calculate whether you can repay an unsecured loan. If the interest rate and monthly payments are too high, you may consider secured loans and contact financial institutions willing to lend you money against security.

Compare Lenders

When you decide to get a personal loan, you will find hundreds of suitable offers on the market. However, don’t hurry to settle for the one you see first.

It is important to compare all the options from reliable and reputable lenders to choose the best one. A loan is your commitment for several years, so always strive to select the options with the lowest interest rate and the lowest monthly payments.

It is also essential for you to understand which financial institution you would like to borrow money from. For example, if you work in the military or are a credit union member, you can approach one and get a personal loan on better terms than a bank.

Read The Terms And Conditions

All the most critical information is always written in small print in the contract, so you must read it carefully. You will usually find additional details about hidden fees and penalties, your rights and obligations, and information about automatic withdrawals.

Be sure to pay attention to the total price of the loan listed in your contract. It often exceeds the amount you planned to see there, so you need to check this point. Also, read in the contract whether your lender reports to all three credit bureaus, as you need this to build a good credit history.

An additional good decision will be to find out if the financial institution has any APR discounts for connecting automatic payments or the ability to reschedule your payments to a more convenient day for you.

Apply For a Loan

Once you have chosen the option that suits you, you need to submit a loan application and provide the company with all the documents required for the contract. Most often, this list includes:

- Passport or driver’s license.

- Proof of your residence (e.g., rental agreement), place of employment, and income level).

- Social Security number.

You will also need to provide your phone number, email, and bank account information. When you submit all this information, the lender will verify it and prepare a loan agreement in a few minutes if your application is approved.

Usually, within a few days of signing the agreement, the company sends the money to your bank account.

Where to Get a Personal Loan

You can get a personal loan online or offline from different financial institutions, depending on how quickly you need the money, what interest rate you agree to, and whether you are a credit union member.

Let’s discuss each option and its pros and cons in more detail to make it easier for you to make your choice.

Banks

Banks provide personal loans at lower interest rates than online lenders. In addition, they often operate in all 50 states and allow you to borrow large sums online and offline. However, this option has a few drawbacks:

- If you are not a customer of the bank you want to get a loan from, you will need to go to one of the branches, which will take longer than applying for a loan online.

- Even if you are a bank user, you won’t always be able to apply online as not all of them allow it.

- Banks usually have stricter requirements for their borrowers, so you must have a good credit score to qualify for their offers.

- If you want to get the borrowed funds into your account, you will have to wait several business days.

Of course, all these disadvantages are unimportant when it comes to security. Many borrowers choose banks for their loans because they are the most reliable lenders and can offer personalized assistance.

In addition, banks offer a lower APR and longer loan repayment terms, so this option is great for anyone who fits their requirements.

Credit Unions

Credit unions are the best place to get loans for most borrowers because they look at a credit score and many other indicators when deciding on loans. People with bad credit scores can get better terms here than in banks or online companies.

However, the main disadvantage of this option is the need to be a member of such an organization to apply for a loan. Those credit unions that offer the most favorable terms are usually reserved for people in certain professions, but some are easy to get into for a small fee.

The pros of this option are as follows:

- You can borrow anything you need, from $1,000 to $100,000.

- Credit unions offer low APRs of up to 20%.

- They consider your credit history and other indicators when deciding on a loan.

As we have already mentioned, the main disadvantage of this option is that you must meet membership eligibility requirements to take advantage of the organization’s offers. Therefore, if you are already a member of such a credit union, make sure you apply to it first.

Online Lenders

Thousands of lenders have entered the financial market over the past 30 years, so it’s becoming increasingly difficult to know which are reliable and which are trying to scam users.

This is both the main advantage and disadvantage of this option – you will have plenty of choices if you want to get a personal loan online, but you could fall into the hands of scammers, who are just as numerous as reliable lenders.

The main pros of online companies that offer the best small personal loans are as follows:

- They save you time, as you can apply in a few minutes and get funds into your account in as little as 1-2 days.

- They rarely conduct hard credit checks and have less stringent requirements for borrowers, which makes it possible to get a loan even for people with bad credit scores.

- You can borrow any amount from them, even $500, for a few weeks.

However, at the same time, it is essential to understand that such financial institutions charge a higher APR and have various additional fees. Therefore, online lenders may be your best choice if you need money urgently and are willing to pay more than a bank.

Peer-to-Peer Lenders

P2P platforms combine borrower applications with lender and investor opportunities. This is usually the principle behind various instant loan apps, which have a database of lenders and allow you to borrow money from them in a few minutes.

The difference between online lenders and P2P websites is slight if these websites operate officially and conduct the application like traditional banks. So what are the advantages of this option?

- You can get a better interest rate than a bank, especially if you have a good credit score.

- You can find a lender willing to lend you money, even if you have a low income or no formal employment.

- Usually, P2P sites do not charge different fees as other online lenders do.

- Obtaining a loan is online and does not take much time.

- You will be able to borrow funds even for business purposes.

Of course, the main disadvantage of this option is the reliability of lenders. Applying to banks, you can be sure that you are in front of a real financial institution, which cannot be said about P2P sites. Always be careful and do not give your information to fraudsters.

Payday Loans vs. Personal Loans

Do you need to borrow a few hundred dollars for 2-4 weeks? Then you need a payday loan. Payday loans and personal loans are both unsecured, but they have many differences, namely:

| Payday loans | Personal loans | |

| Borrowing amounts | $50, $100, $200, $300, $500 | $1,000, $1,500, $2,500, $3,000, and up to $100,000 |

| Repayment terms | from 2 to 4 weeks until your next paycheck | from 2 to 10 years |

| APR | up to 800% | up to 36% |

| Impact on credit | have no impact, if your lender doesn’t report to the credit bureau | can help you build credit, if you make your payments on time |

| Pros | (+) Easy to qualify even with a bad FICO score

(+) Lenders often do not conduct credit checks (+) You can receive funds in several hours |

(+) Personal loans have lower APR

(+) You can borrow any amount you need (+) You can receive money into your account in 1-3 days |

| Cons | (-) High APR and fees

(-) Small repayment term |

(-) Harder to receive because of requirements |

Opt for personal loans whenever you have the opportunity, as they are safer. However, payday loans are meant for the low-income category; their high APR often leads borrowers into debt.

What to Consider Before Taking Personal Loans

Before you apply for a loan, you should ask yourself the following five questions:

How much money do you need to borrow? Be sure to calculate the amount you need and include the origination fee.

What monthly payment is convenient for you? For example, if you can make a monthly payment of $300, you should start saving that amount immediately. Even if your monthly payment with the most advantageous lender is $250, paying $50 more each time will help you repay your loan faster.

Can you stick with the payment plan for the next few years? So many borrowers need to remember that a loan is a long-term commitment and should not be taken on if you have an unstable job and no savings.

Do I have a good enough credit score? Remember that even 50 FICO points can change your interest rate and save you hundreds of dollars over a year. So it may make sense to put off getting a loan for six months if your score is too low and work on improving it during that period.

Do I need this loan? Unfortunately, many people’s mindset is adapted to taking out loans rather than earning their desires. Consider whether you can buy what you want without a loan but with your income. This may be your motivation to increase your revenue.

Pros and Cons of Personal Loans

As we have already mentioned, such loans are the most popular worldwide. This is because they are convenient, they are easy to get, and they also have many advantages:

- You can use a personal loan for almost any legitimate purpose.

- You can expect a lower APR than credit cards and other types of credit if you have a good FICO score.

- These loans are regulated by law, unlike payday loans.

- You can get almost any amount you need if you turn to personal loan lenders.

- You do not have to provide collateral if you do not want to, as most of these loans are unsecured.

- You can use them to build your credit history if you make your monthly payments on time.

- If it is unsecured, you can get a personal loan in just a few days.

- You can plan a repayment schedule for the borrowed funds even before you receive them, as they have a fixed interest rate.

However, at the same time, this option of borrowing has several disadvantages. For instance, they have high fees and penalties, especially for borrowers with low FICO scores.

Furthermore, unlike credit cards, they require regular monthly payments, which can make your total debt grow. In addition, if you suddenly fail to repay the borrowed funds on time, you may face severe consequences and financial difficulties.

Overall, personal loans are a great option to buy something that you can’t afford but want or need. You have to borrow precisely how much you can pay back over time, so your credit history consists only of positive marks.

FAQ

How to get a personal loan instantly?

Most of the time, it will take you one to 7 days to get an unsecured loan. To get the loan faster, you can approach a lender who can transfer the funds in just a few hours for a small express fee. Another option that you can use in this situation, you can borrow funds in a couple of hours to get a loan offline at one of the lender’s branches.

How many personal loans can I have at the same time?

The law does not limit the number of personal loans you can have at any one time, so you can approach lenders as often as you need. However, remember that they look at the debt-to-income ratio to determine if you can pay off another loan, so you can’t borrow an infinite number of them.

What are the best lenders for personal loans?

If we talk about banks, Discover, American Express, Wells Fargo, and Citibank have the best conditions for personal loans, as they do not charge origination fees and offer low interest rates. As far as online lenders are concerned, users respond well to SoFi, Upgrade, and LendingClub.

Whether I am eligible to get a personal loan with bad credit?

Many lenders on the market work with these borrowers, so your low FICO score will ensure you get a loan. You may need proof of income or formal employment to borrow money, but you can still qualify for at least a secured personal loan.

How high are the fees on personal loans?

The most oversized fee many lenders charge is an origination fee of 1% to 10% of the amount borrowed. They may also charge prepayment or late fees if you decide to pay early or miss a monthly payment, but they are usually at most $30.

When do I need a personal loan?

You can always get a personal loan if you want to buy but don’t have enough money or borrow money to cover unexpected expenses. This will allow you to get funds within a few days at an interest rate of up to 36% per annum. However, you do not need to apply for a loan if you are not sure you will be able to repay the borrowed money on time.

How to get a personal loan with no credit check?

You can apply to lenders that don’t do credit checks, such as credit unions or some online companies. In addition, some applications allow you to borrow a small amount of up to $500 without checking your credit rating.